Is the Future of Banking in Underserved Markets?

For financial institutions under pressure to grow while meeting regulatory expectations and deepening community impact, one reality is becoming clear: The future of growth in banking will be driven disproportionately by Hispanic consumers.

As seen in our 2025 Hispanic Market Report, Hispanics already represent more than 20% of the U.S. population and are expected to drive 80% of population growth through 2031. At the same time, the non-Hispanic White population is declining as a share of the total population, meaning growth strategies anchored in the “general market” are increasingly misaligned with reality.

For banks and credit unions pursuing CDFI certification, this goes beyond a demographic shift – it’s a measurement challenge, a segmentation inflection point and, ultimately, a growth strategy imperative.

From Market Share to Cultural Membership

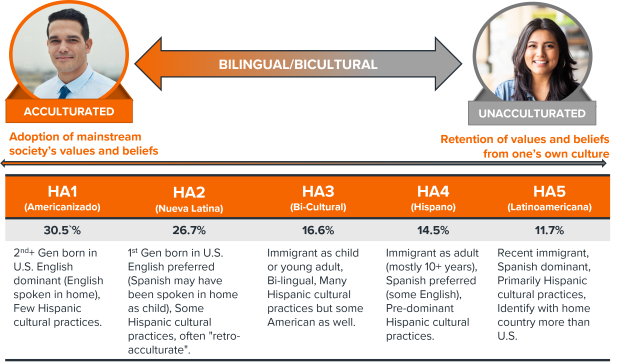

Many institutions still only evaluate Hispanic engagement through surface-level indicators ranging from campaign reach to Spanish-language adoption or even branch placement, but the data tells a deeper story. It’s important to remember that just like all cultural groups, the Hispanic market is not monolithic, with differences in acculturation, language, and behavior requiring more precise approaches.

This is where cultural membership benchmarking becomes critical.

Instead of asking, are we reaching Hispanic consumers? leading institutions are asking, are we relevant to Hispanic consumers and do they see us as a financial partner for their community?

This distinction matters because:

– More than 70% of Hispanic adults are either English dominant, preferred or bi-lingual, navigating fluidly between languages and cultural contexts

– Hispanic consumers are deeply influenced by bicultural identity and community orientation

– Growth is increasingly driven by younger, digitally engaged, culturally connected segments

Cultural membership, then, becomes a leading indicator of performance – one that directly impacts acquisition, retention, and lifetime value.

One way to grow cultural membership is through efforts, like bi-literacy. If your branches are located in highly concentrated Hispanic markets, it’s not enough to support with tellers and lending officers that are bi-lingual, you need to understand the investment needed for bi-literate employees to accurately explain financial product offerings and terms and conditions to the members.

The CDFI Balancing Act: Growth vs. Mission Integrity

For Community Development Financial Institutions (CDFIs), the opportunity and challenge are even more pronounced. CDFIs are inherently aligned with Hispanic communities, but they now face two converging pressures:

– Demonstrating measurable impact to maintain certification and funding

– Achieving aggressive growth targets to remain sustainable and competitive

The Hispanic market offers a path to both, but only if institutions can prove they are reaching and serving these communities effectively.

Consider the scale of the opportunity:

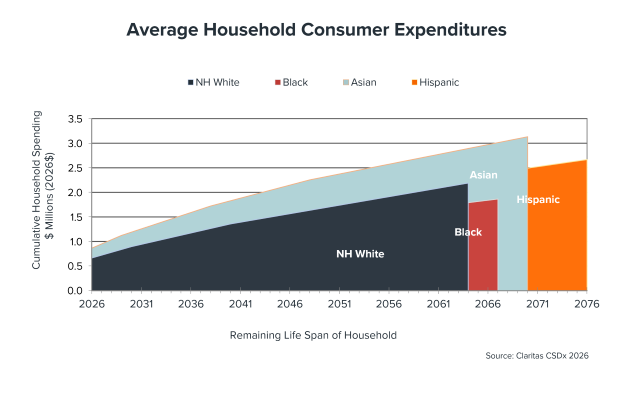

-The average Hispanic household will now spend approximately $2.7M over their remaining lifetime

– The U.S. Hispanic population has accounted for the majority of population growth since 2010

For CDFIs, growth isn’t just about generating more loans, it’s about putting money into the right communities in ways that actually match their needs and values.

Institutions that rely solely on geography or income thresholds risk missing high-potential households within Hispanic communities while also falling short in demonstrating meaningful inclusion.

Why A Strong Segmentation Strategy is a Strategic Requirement

When it comes to audience targeting, two fundamental truths have become very clear: broad assumptions no longer work, and success depends on how precisely you understand and reach the right consumers.

Hispanic consumers differ significantly across:

– Financial behaviors (credit usage, savings patterns, entrepreneurship)

– Life stages (first-generation wealth builders vs. established households)

– Cultural orientation (language preference, acculturation, identity)

At the same time, the opportunity is enormous:

– Hispanic households skew younger, which creates long-term customer/member lifecycle potential

– They are driving adoption in mobile, streaming, and digital-first environments

This is where a strong segmentation strategy becomes essential.

Remember earlier when we warned against treating Hispanic consumers as a monolith? Leading institutions already know this and are using segmentation frameworks that combine:

– Financial capacity and product needs

– Household composition and multigenerational dynamics

– Cultural engagement and communication preferences

This enables more effective strategies such as:

– Identifying emerging mass-affluent Hispanic households for wealth-building products

– Supporting thin-file or credit-invisible consumers with tailored lending

– Designing small business and entrepreneurial banking solutions

For CDFIs, this precision supports both portfolio performance and certification alignment, demonstrating impact at a deeper, more measurable level.

Multigenerational Households Are Changing the Growth Equation

One of the most important, but underutilized, insights in the Hispanic market is the prevalence of multigenerational households.

Financial decisions are often made collectively, influencing:

– Product adoption across multiple generations

– Shared financial goals (homeownership, education, family support)

– Cross-product relationships within a single household

This shifts the growth model for financial institutions. Instead of focusing on individual account holders, institutions must think in terms of household lifetime value, which is significantly amplified in Hispanic communities.

Digital Behavior Is Accelerating the Shift

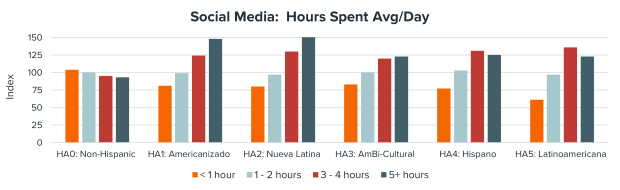

Hispanic consumers are not just participating in digital; they are leading it.

As highlighted in the U.S. Hispanic Market Report, these consumers represent strong engagement across:

– Mobile platforms

– Streaming and connected TV

– Social and messaging ecosystems

This is driven in part by younger demographics and bilingual, bicultural behaviors that adapt quickly to new platforms.

For financial institutions, this creates a clear mandate:

– Digital is the primary relationship channel, not a secondary one

– Engagement must be culturally relevant, not just accessible

Institutions that fail to deliver seamless, mobile-first, culturally aligned experiences risk losing share, especially among younger Hispanic consumers entering the financial system.

Testing Smarter: How AI Optimization Is Changing Campaign Performance

Reaching a digitally savvy, bilingual, and culturally dynamic audience requires more than just showing up on the right channels, it requires continuously learning what resonates.

This is where many financial institutions are beginning to test AI-driven campaign optimization.

Rather than relying on static audience definitions or one-size-fits-all creative, AI-powered tools can:

– Dynamically adjust targeting based on real-time engagement signals

– Optimize messaging variations across language, tone, and cultural cues

– Identify high-performing audience segments that may not be obvious through traditional analysis

– Continuously improve media efficiency across mobile, streaming, and social environments

For Hispanic audiences where behavior, language preference, and cultural identity can shift fluidly, this level of adaptability is especially valuable. It also creates an opportunity to move beyond assumptions.

Instead of guessing which messages will resonate with different segments, institutions can test, learn, and refine in real time, building campaigns that are both data-driven and culturally relevant.

For CDFIs and growth-focused institutions alike, AI optimization offers a way to:

– Stretch limited marketing budgets further

– Improve acquisition among high-potential but hard-to-reach segments

– Demonstrate measurable improvements in engagement and conversion

In a market where precision is everything, the ability to continuously optimize is quickly becoming a competitive advantage.

A New Standard for Growth, Measurement, and Accountability

As the Hispanic market becomes the dominant driver of U.S. growth, financial institutions must evolve how they define success.

It is no longer enough to track:

– Accounts opened

– Loans originated

– Campaign performance

Institutions must also measure:

– Cultural membership and trust

– Segment-level performance within Hispanic communities

– Alignment between growth and community impact

For CDFIs, this is particularly critical. The ability to connect who you serve, how you serve them, and the outcomes you drive will play a central role in sustaining certification and attracting capital.

The Path Forward

The Hispanic market is not an emerging segment; it is the primary growth engine of the U.S. economy.

With Hispanics driving 80% of population growth, contributing millions in lifetime household spending, and reshaping digital and financial behaviors, the opportunity is both immediate and long-term.

Financial institutions that invest in:

– Cultural membership benchmarking

– Advanced financial segmentation

– Digitally driven, culturally relevant engagement

…will be positioned to meet growth goals while strengthening community impact. Those that don’t may find themselves competing harder for a shrinking share of the market.

The opportunity is clear. The data is undeniable. The only question is whether your strategy and your measurement framework has caught up. To learn more about the data cited in this article access a complimentary copy of The 2025 U.S. Hispanic Market Report from Claritas, here.

This article was originally written for and published on The Financial Brand’s website.

Need help finding your next customer?

Questions

Please contact the Claritas Sales Team at866-ROI-TEAM (866-764-8326)

Current Clients

Please contact the Solution Center at855-400-ASST (855-400-2778) for immediate assistance